Economic Pulse: Job Market, Housing Trends, and Fed's Rate Hike Plan

Hot Job market numbers, Student loan resumption, Fed's Rate hike plan

Great news! The SettleWise newsletter subscriber base has doubled in just a few weeks. We are grateful for your support in making this possible. Let's continue growing our community and helping more immigrants by sharing the newsletter.

Share the knowledge, grow the community, empower each other!

Economic Pulse: Job Market, Housing Trends, and Fed's Rate Hike Plan

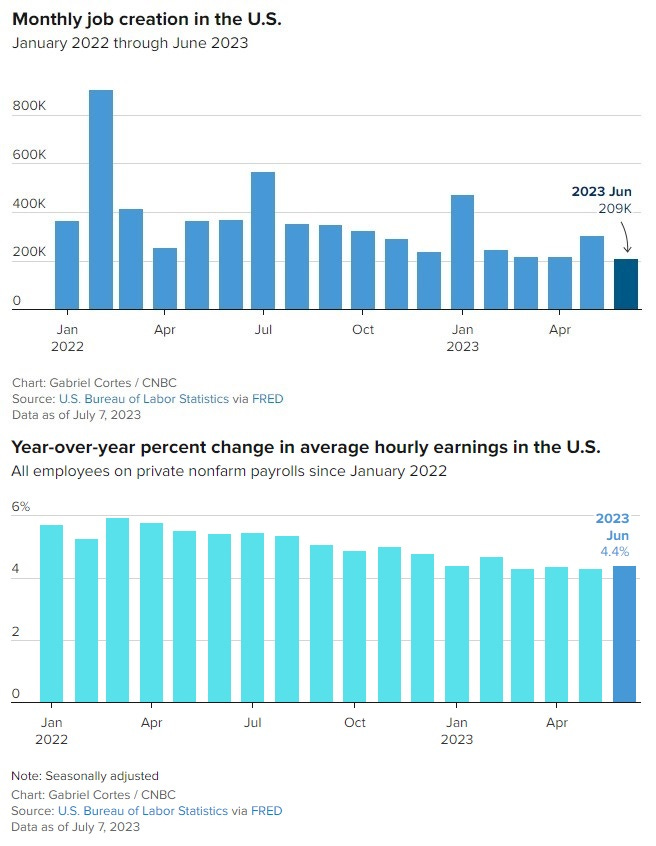

Nonfarm payrolls increased 209,000 in June, below the consensus estimate for 240,000.

The unemployment rate was 3.6%, down 0.1 percentage point. However, a more encompassing jobless level rose to 6.9%.

Government hiring led the job gains, followed by health care, social assistance and construction.

Wages rose 4.4% from a year ago, slightly higher than expectations.

In June, hiring slowed as the Federal Reserve's efforts to combat inflation showed signs of taking hold. However, despite concerns about a possible recession, the labor market remains resilient with rising wages and low unemployment. The latest report from the Labor Department revealed that U.S. employers added 209,000 jobs, marking the 30th consecutive month of payroll gains. Although this figure represented a cooling trend compared to the previous month, it is important to note that the numbers are seasonally adjusted.

ADP reports the U.S. labor market continued to show strength as private sector jobs surged by 497,000, surpassing expectations. The increase was the largest monthly rise since July 2022 and well above the consensus estimate. Leading the way were the leisure and hospitality sector with 232,000 new hires, followed by construction with 97,000, and trade, transportation, and utilities with 90,000. However, while job creation remained strong, wage growth in consumer-facing service industries has been slowing. Despite a year of Federal Reserve interest rate increases aimed at cooling the job market, there are still nearly two open positions for every available worker. This unexpected jump in payrolls suggests ongoing resilience in the U.S. labor market, even amid concerns about inflationary pressures. This fuels the Fed's view to continue its aggressive interest rate hikes, which will, in turn, impact mortgage rates and housing affordability. The 30-year fixed mortgage rate jumped to 7.22% on Thursday. That's a new 2023 peak, driven by strong economic data and expectations the Fed will keep hiking rates. In recent days, Fed officials have provided indication that more rate hikes are likely even though they decided against moving at the June meeting.

Markets widely expect a quarter percentage point increase in July that would take the Fed’s benchmark borrowing rate to a targeted range between 5.25%-5.5%. The outlook was little changed following the jobs data release, with traders pricing in a 92.4% chance of a hike at the July 25-26 meeting.

According to FS Investments' chief market strategist, Troy Gayeski, US stocks could potentially crash by 25% from their current levels if the Federal Reserve continues its aggressive interest rate hikes. Gayeski believes that these monetary tightening measures could lead to a recession in the fourth quarter of the year. He suggests that the economy, which was not a concern earlier, now poses one of the biggest threats to equity prices and valuations over the next three to six months. Gayeski gives odds of 70% to 80% for a recession before the end of 2023. The Fed's interest rate hikes aim to combat rising inflation, but higher borrowing costs tend to lower spending levels, affecting economic growth. If the US jobs market contracts, it could signal a full-blown recession and potentially trigger a stock market crash. While inflation may stabilize, a recession is not favorable for earnings or revenue.

The Supreme Court's decision to strike down President's program for student loan debt forgiveness could have negative consequences for both individual borrowers and the U.S. economy. The ruling means that billions of dollars of consumers' disposable income will be taken out of circulation, potentially resulting in a "modest headwind" against economic growth. Economists estimate that the resumption of student loan payments will divert around $73 billion annually, representing 0.27% of the country's GDP. The impact on the economy is not expected to lead to a recession but is still a significant hit. Some economists believe that the resumption of loans could be the tipping point that triggers a recession, particularly considering the current state of consumer spending and diminished savings during the pandemic.

#SettleWiseStance – The resumption of student loan payments, which will divert big money, could potentially have an impact on car loan and housing mortgage defaults. When borrowers have additional financial obligations, such as student loan payments, it can strain their overall budget and potentially affect their ability to meet other financial commitments.

If individuals are already experiencing financial challenges or have limited disposable income, the added burden of student loan payments could increase the risk of default on car loans or mortgages. It could result in some individuals struggling to make timely payments, leading to delinquencies or even defaults.

However, the extent of the impact will depend on various factors, including the individual's financial situation, income stability, and overall debt load. Additionally, other factors such as interest rates, employment levels, and economic conditions can also influence loan defaults. Keep an close eye on these things and take an informed decisions either you are buying a car or a home, or planning to invest.

Wiser Craving

Multiple subscribers reached out expressing their interest of learning few specific topics. If you want to read about any specific topic, Please let me know in the comments or email to author.settlewise@gmail.com

#WiserCraving Topic of this edition is $100K ≠ $100K.

$100K ≠ $100K

Having a $100,000 is not the same in California as it is in Texas. With the high cost of living in California, including housing, taxes, and other expenses, the purchasing power of $100,000 is significantly lower compared to Texas, where living costs are generally more affordable ( I know TX is not cheap 🤪. This is just comparing with CA).

Whether you're a first-time job seeker in the USA or planning to relocate within the country, effectively comparing salaries is crucial. Evaluating salaries based on cost of living and purchasing power parity (PPP) helps determine the real value of compensation in different locations. This article explores how job seekers can make informed salary comparisons, highlighting the usefulness of these strategies for those entering the job market for the first time and individuals seeking to relocate within the USA.

To compare salaries by location, job seekers can consult reputable websites that provide median salary information. Some reliable platforms include:

Glassdoor (https://www.glassdoor.com/Salaries/index.htm)

Indeed (https://www.indeed.com/salaries)

Levels (https://www.levels.fyi)

These websites offer comprehensive salary data based on location, industry, job title, and experience level, allowing job seekers to make more informed salary comparisons.

To evaluate the real value of salaries based on cost of living and PPP, job seekers can refer to the following websites:

Numbeo (https://www.numbeo.com/cost-of-living): Numbeo provides extensive data on cost of living, including rent, groceries, transportation, and more, allowing users to compare expenses between locations.

Expatistan (https://www.expatistan.com/cost-of-living): Expatistan offers a cost of living comparison tool that allows users to compare the cost of living in different cities worldwide, considering various expense categories.

World Bank Data (https://databank.worldbank.org/): The World Bank provides data on PPP, allowing users to understand the relative purchasing power of different currencies across countries.

#SettleWiseStance – By combining median salary data, cost of living information, and PPP analysis, job seekers can gain a comprehensive understanding of the financial aspects associated with job opportunities in different locations. Remember, salary is just one piece of the puzzle—considering cost of living and other factors will help you make a more well-rounded decision. Leverage the websites mentioned in this article to empower your job search and find the right fit for your career and lifestyle.

Building a Strong Credit History and Pitfall Avoidance

Having a strong credit history is crucial for settling in USA. It opens doors to favorable interest rates, loan approvals, and other financial opportunities. However, building credit requires responsible habits and avoiding common pitfalls. In this article, we will explore strategies to establish and maintain a strong credit history while highlighting key pitfalls to avoid along the way.

Establishing Credit:

Open a Starter Credit Account: Begin by applying for a credit card or a secured credit card, designed for those with limited or no credit history. Make small, regular purchases and pay off the balance in full each month to establish a positive payment history.

Become an Authorized User: Ask a family member or close friend with a good credit history to add you as an authorized user on one of their credit accounts. Ensure that the account has a positive payment history and low credit utilization to benefit from their responsible credit habits.

Building Credit Responsibly:

Make Timely Payments: Pay all your bills, including credit cards, loans, and utilities, on time. Late or missed payments can have a negative impact on your credit score.

Keep Credit Utilization Low: Aim to keep your credit utilization, which is the percentage of available credit you use, below 30%. High credit utilization can signal financial risk and negatively impact your credit score.

Diversify Your Credit Mix: Consider having a mix of credit accounts, such as credit cards, installment loans, and a mortgage if applicable. This demonstrates your ability to handle different types of credit responsibly.

Pitfalls to Avoid:

Overspending: Avoid maxing out your credit cards or accumulating excessive debt. Practice responsible spending within your means to maintain a healthy credit-to-debt ratio.

Late Payments: Consistently paying bills late or missing payments can significantly damage your credit score. Set up reminders, automate payments, or use budgeting tools to stay on top of your financial obligations.

Applying for Multiple Credit Accounts: Avoid applying for multiple credit cards or loans within a short period. Each application triggers a hard inquiry on your credit report, which can temporarily lower your credit score.

Closing Old Credit Accounts: Closing old credit accounts, especially those with a positive payment history, can reduce your overall credit age and impact your credit score negatively. Instead, keep those accounts open and active with occasional use.

#SettleWiseStance – It is advisable not to close the oldest credit card account solely due to a lower cash back percentage. If the account has no annual fee, it is beneficial to keep it open and use it at least once a year to maintain activity. Additionally, when purchasing your first car, consider opting for an auto loan instead of paying in cash. This decision contributes to a diversified credit mix. Aim to keep credit utilization below 10% by paying off the balance before the billing cycle and ensuring that the bill amount remains under that threshold. Maximizing cash back rewards while maintaining a low credit utilization is a smart credit card trick. By strategically paying off the balance before the billing cycle and keeping the bill amount below 10%, you can enjoy the benefits of cash back while showcasing responsible credit management.

If you have any further question, please ask it in the comments or email to author.settlewise@gmail.com . SettleWise team will try to get the answer for you.

Idioms and Phrases

Plenty of fish in the sea - there are plenty of other opportunities out there

Beef up - to strengthen something

Earworm - thinking about a song or lyrics from a song over and over

Quit cold turkey - to give up something all at once rather than gradually weaning off it

Zebras don't change their stripes - don't expect anyone to be anything other than who they really are

We value your feedback! Please take a moment to share your thoughts on this episode and let us know what topics you would like to read about next. Your input guides us in delivering valuable and relevant content. Feel free to leave your feedback in the comments below.

Thanks for reading SettleWise! Was this email forwarded to you? That's wonderful! It shows how much they value you and believe that you would benefit from the content. Subscribe for free to receive new posts and support my work.

Disclaimer: I am not a certified professional in the fields discussed. The content provided in this article is for educational and entertainment purposes only. The opinions and suggestions shared are intended to provide general information and assist you in making informed decisions. Please note that while I may mention specific products or services, I may earn referral income from some of the links provided, but no additional cost to you. Therefore, while you can continue reading and absorbing the information, please exercise your own judgment and seek professional advice when necessary.